Part 13 of the Notes from the Field series discusses the Narrative Machine, which can help us see the invisible memes that drive our political behavio…

The inevitable result of financial innovation gone awry, which it ALWAYS does, is that it ALWAYS ends up empowering the State. When too clever by half…

What if I told you that the dominant strategies for human investing are, without exception, algorithms and derivatives? I don't mean computer-driven i…

The pecking order is a social system designed to preserve economic inequality: inequality of food for chickens, inequality of wealth for humans. We ar…

In Part 6 of the Notes from the Field Series, Ben observes that we think we are wolves, living by the logic of the pack. In truth we are sheep, living…

In Part 4 of the Notes from the Field Series, Ben identifies how the natural lines of a tree and shaping the tree to follow those lines over time is a…

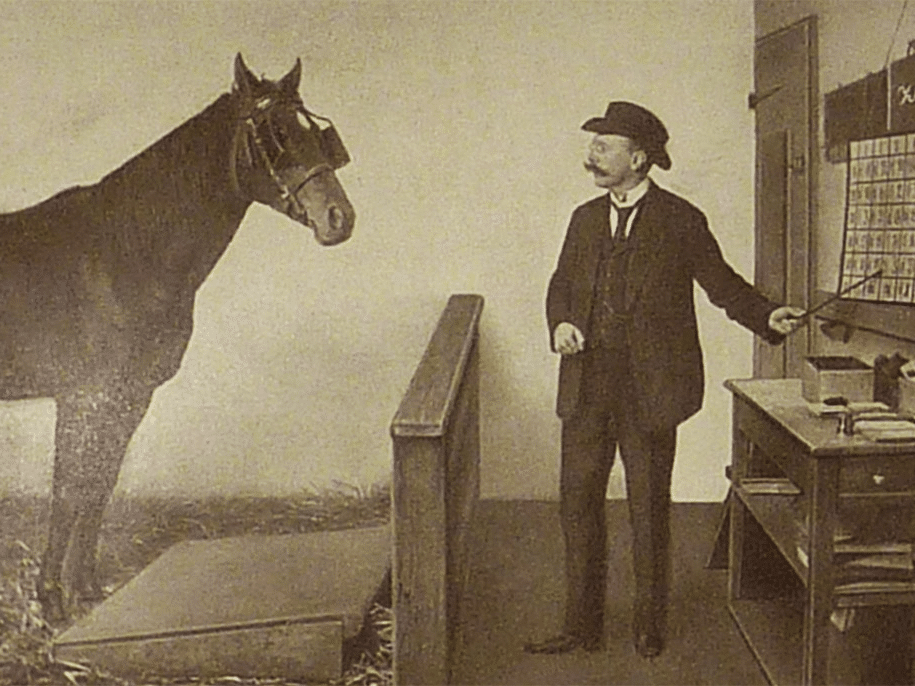

There is no animal more important to the ascendancy of Western Civilization than the horse, and no invention more important than the horse collar. Aft…

Part 2 of Ben's Notes from the Field series, in which he considers the question: what can a bird teach us about value investing? To everything there i…

What does farming have to do with investing? Quite a lot, actually. In this first of a series that takes on a life of its own, Ben discusses bees and …

We use cookies to optimize our website and our service.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.