The dominant COVID-19 narrative today is a "short and deep" economic impact, with a corollary narrative of "pent-up demand". These are market-positive…

At the request of some ET Pro subscribers, we explore current Big Tech Monopoly narratives. We find an increasingly cohesive, negative narrative that …

In this ET Pro In Focus note, we explore the narrative structure of ESG and SRI investing. Our question: is it finally part of the Zeitgeist, or a tre…

For fund managers and asset management executives, the fundraising question is often the most important and most inscrutable. Understanding how narrat…

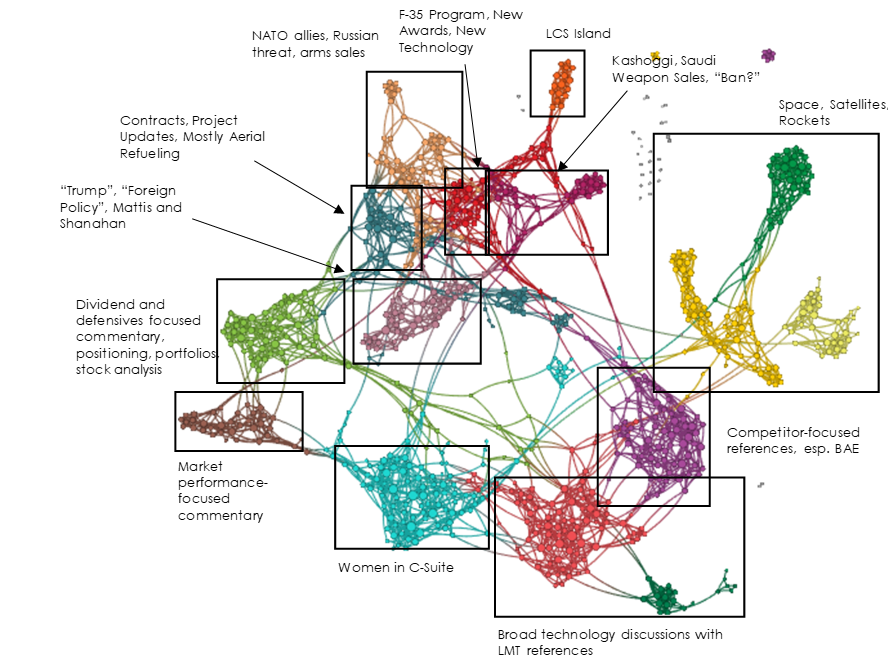

With aerospace and defense in the spotlight, we turn our own spotlight to the sector. We find a generally weak narrative structure with a lot of vulne…

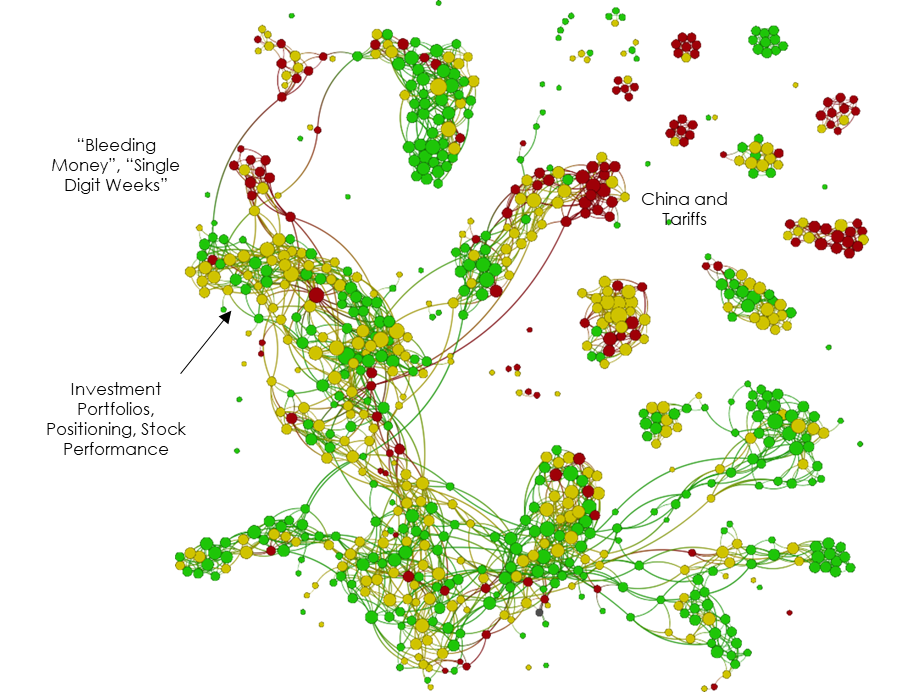

US Banks have a common narrative structure - two competing topics of vastly different sentiment, with one dominating market attention at any given tim…

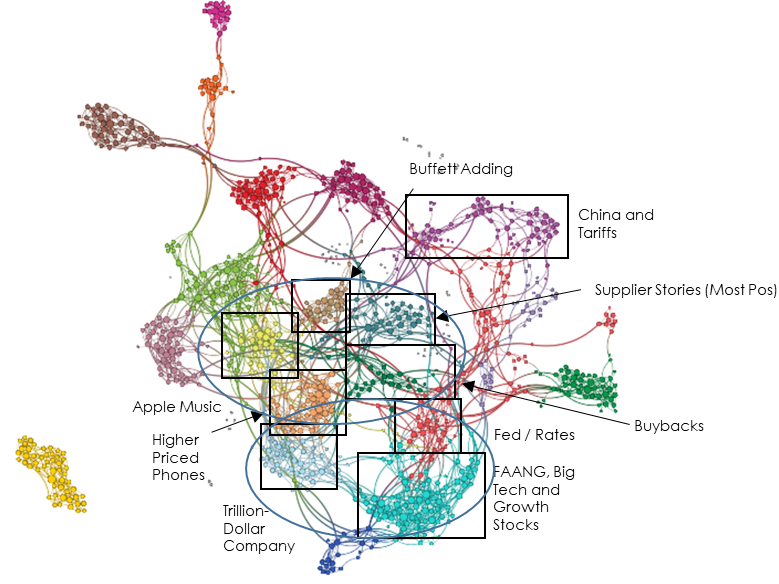

We examine how Apple found both of the ways to lose on narrative in less than two months' time, and outline how that might change the playbook for the…

With increasing attention to trade and tariff narratives and falling attention to inflation and growth narratives in the U.S., we believe that investo…

With some breathing room following an eventful earnings call, we re-examine the narrative around Tesla, and consider whether it has successfully navig…