Things That Go Bump In The Night

Everyone reading this note has, at one time or another, gotten scared about markets and decided to hedge their professional portfolio or personal acco…

“No wonder kids grow up crazy. A cat’s cradle is nothing but a bunch of X’s between somebody’s hands, and little kids look and look…

Portion of original dot map by Dr. John Snow, the founding father of epidemiology, showing the clusters of cholera cases in the London epidemic of…

BOTOX® is the only FDA-approved, preventive treatment that is injected by a doctor every 12 weeks for adults with Chronic Migraine (15 or more headache…

Campaign Company Launch Date “Flo” Progressive Insurance 2008 “Rhetorical Question” “Happier Than A … ” “Did You Know?” “It’s What You Do” GEICO 2009 2012…

As longtime Epsilon Theory readers know, I’m a big comic book fan. One of the joys of a comic done well is the effective representation…

Kilgore: Smell that? You smell that? Lance: What? Kilgore: Napalm, son. Nothing else in the world smells like that. – Apocalypse Now (1979) Hello, hello, hello,…

Unfortunately for mariners, the total amount of wave energy in a storm does not rise linearly with wind speed, but to its fourth power. The…

Sen. Geary: Hey, Freddie, where did you find this place? Fredo Corleone: Johnny Ola told me about this place. He brought me here. I didn’t…

Mike McDermott: In “Confessions of a Winning Poker Player,” Jack King said, “Few players recall big pots they have won, strange as it seems, but…

When I look over my shoulder What do you think I see? Some other cat lookin’ over His shoulder at me. – Donovan, “Season of…

The Three Types of Fear: The Gross-out: the sight of a severed head tumbling down a flight of stairs. It’s when the lights go out…

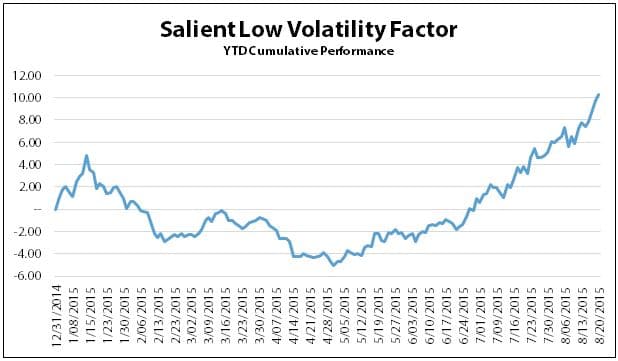

War is too important to be left to the generals. – Georges Clemenceau (1841 -1929) Competition has been shown to be useful up to a…