Every morning, we run The Narrative Machine on the past 24 hours worth of financial media to find the most on-narrative (i.e. interconnected and central) stories in financial media. It’s not a list of best articles or articles we think are most interesting … often far from it.

But for whatever reason these are articles that are representative of some sort of chord that has been struck in Narrative-world.

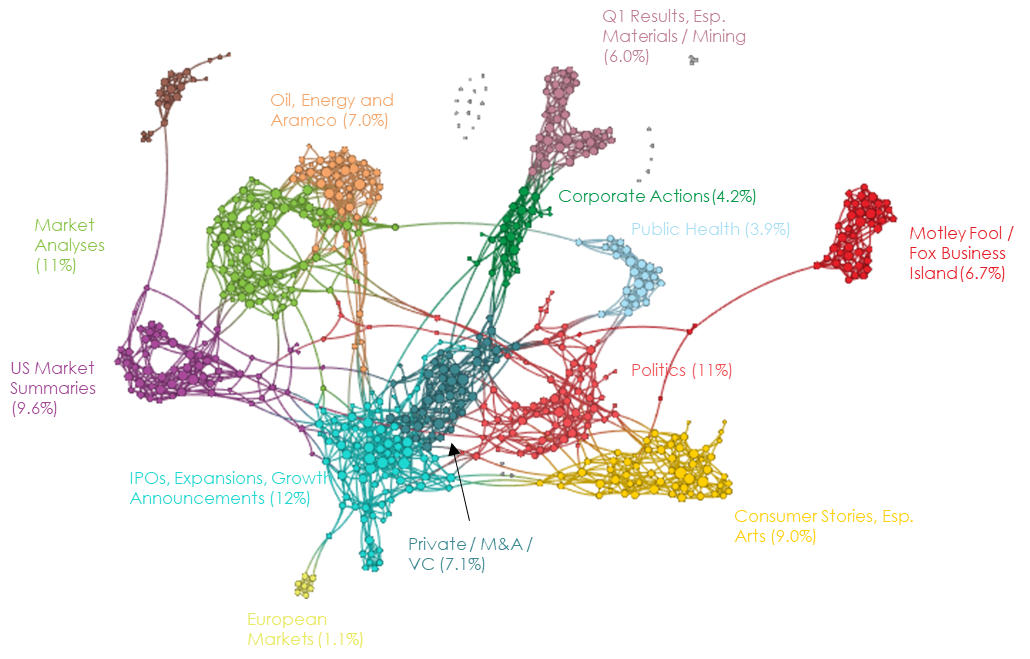

April 15, 2019 Narrative Map – US Equities

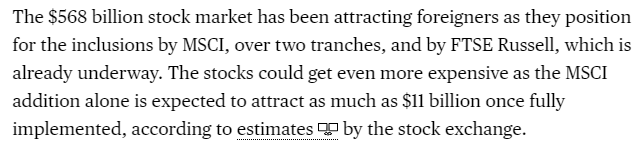

Investors Joining Saudi Stocks’ Big Moment Have to Pay a Premium [Bloomberg]

We rightfully emphasize the supreme importance of our asset allocation decisions. Yet as a group, we investors tend to apply an uncritical eye to asset classes, and accept them as they come to us. Questions we rarely ask in more than a perfunctory manner: Do they refer to any sensible organization of securities with similar underlying traits? Are they subject to features at the arbitrary power of an organization deciding where they belong? Does Saudi being moved from one index to another matter (yes!). Should it (no!)?

We will be writing a lot more in the coming months about how we think untethering from index provider-based constructs for asset classes will be an increasingly important asset allocation tool in the emerging Zeitgeist.

PG&E, BlueMountain in Talks Over Board Composition [Reuters]

I’m on record saying that one of my bigger manager diligence whiffs was not investing with ValueAct for what seemed to me to be good reasons at the time (i.e. small cap specialist with mission creep into mid- and big-caps, a very right-sounding story). They have done very nice work for their investors.

But I will never not hear of a nomination of Jeff Ubben to a board without playing the game I call “Jeff Ubben or Aaron Eckhart from Thank You For Smoking?”

Deutsche Bank-Commerzbank Deal May Rest on a Mountain of ‘Badwill’ [Dow Jones]

Yes, this is all very stupid, but look, ensuring the stability and liquidity of the most critical bank in the most important European economy DOES fall pretty squarely within the mandate of the ECB. As ridiculous as this sounds on paper, it is frankly a lot less ridiculous than some other things being considered. Still, ‘can we immediately capitalize the fact that the market knows we’re going to piss away the ‘value’ of these assets over time into a gain to help our capital ratios’ is a pretty bold move, Cotton.

Will Wall Street Lose Faith in Eager-to-Please Fed? [New York Times]

I believe this is the first use of ‘[The Fed] is out of bullets’ in a major publication in 2019. It is truly a red-letter day. Those of you in God’s Country may discharge your firearms in the air in celebration. The rest of you may non-threateningly wave a knife or other sharp object of less than 5″ in total blade length.

Europe putting venture capital back in the game [P&I]

We have covered the ebullient narratives about private equity and venture capital at some length over the last few months, especially in comparison to those no-good scoundrels in hedge funds. The Billions-Silicon Valley Effect, if you will (sorry, but except for punching that guy who drove your kid drunk, you’ve done hedge funds no favors, Captain Winters). It is easy to look at a story like this and conclude that it’s a secondary effect of too much capital chasing too few remaining opportunities. Everyone wants to get their big unicorn pop before it’s too late to make a career off of it.

And yet I will tell you this: If you want a dependable canary in the coal mine for what other big state, municipal and government pensions will do, you can do far worse than to watch what OMERS does. There is about a trillion of US pension money that relies on the freedom granted by OMERS’s management company structure (and that of a few similarly situated peers) to provide ‘legitimacy’ cover for things they want to do but can’t be the first.

Goldman Economists Say Trump Re-Election More Likely Than Not [Bloomberg]

If this were a live feature, I would allow you to select from an economist joke, a Goldman joke, or a Trump joke in this place. Instead, in the spirit of greatest movie celebrating the very in-the-current-Zeitgeist game of golf, you’ll get nothing and like it.

Everyone’s Income Taxes Should Be Public [New York Times]

Appelbaum’s arguments in favor of destroying the last vestiges of privacy in America all boil down to the same very dumb argument: ‘But think of what we could do with all the data!’

It’s the same reason that free Facebook exists, and free Twitter, and every other service in which you, dear reader, ARE the product because of the value of your data. But instead of advertisers, the consumers of the Product of You in Appelbaum’s world are academia, special interest groups, pitchfork mobs, employers, neighbors with grudges, University admissions offices, lending institutions and journalists who have run out of Twitter posts from random accounts to build feature stories around. Think you get a lot of junk mail and robo-calls now? Think bigotry in lending, housing and admissions is a problem now? Think gerrymandering and selective doling out of local resources is a problem now? Think politically motivated use of the IRS and other government investigative agencies is a problem now? Think widespread depression and anxiety are problems now? Think political races go petty, personal and dirty now? Think the number of political and social ideas to engineer a society in one group’s image is dangerous now? Think the way in which missionaries work to divide us is perilous now?

If the hilariously predictable outcomes were not enough, the justification provided is even flimsier. “Income taxation is an act of government.” Please. If that were the nexus that justified public disclosure, then we ought to disclose the detailed records of every health service, diagnosis and prescription by individual affected by an ‘act of government’. Same for the transcripts and disciplinary records of every student at a public school or school receiving public funding. Hell, those would be GREAT datasets!

The fact that one is forced by threat of imprisonment into a transaction with the state doesn’t inherently warrant public disclosure. Nor does the usefulness of that data. Render your taxes unto Caesar – but keep the data about them to yourself.

Re: asset allocation, one of the things I have become more attuned to lately is how our conception of asset classes is influenced by the type of exhibit used to visualize the allocation. If you put categories on a page, and make them appear finite and distinct, people will think of them as finite and distinct, regardless of whether that distinction is borne out in the behavior of those securities. E.g. you can say Small Cap US Equity is a thing or SMID Cap US Equity is a thing. Is that distinction at all meaningful in terms of the ultimate drivers of risk and return in the portion of the allocation? I would argue no.

When I think about the stereotypical diversified wirehouse or RIA portfolio, for example, it basically rolls up into US Equity beta (MAYBE Global Equity beta if the FA is a glutton for punishment) plus Duration beta plus Credit beta. The fancy allocation exhibits are just window dressing.

Agreed. And as Ben said in an ET note I love “Don’t Fear the Reaper:”

“I think that there is enormous room for improvement in constructing smart portfolios if we can stop staring at surface appearances and start focusing on the investment DNA of securities and strategies.”

Deeply thinking about the “DNA of securities and strategies” is one way to meaningfully improve your performance. I’d go further and say you’ve been committing portfolio malpractice if you haven’t always been doing this.

Regarding Deutsche Bank, etc., how is it that Europe’s only strong economy hasn’t any strong banks (of any significant size)? Is the economy not really strong or did something go wrong in the German approach to banking?

Regarding Goldman’s call: I will not read, listening to or allow to penetrate my consciousness any calls on “who will win in 2020” for, at least, another year and, then, I’ll hate myself for doing so.

Regarding tax returns being made public: besides the arrogantly obnoxious loss of privacy, is there any sentient being that doesn’t see that as a way to widen the gyre to the breakpoint - which just might be the reason as, to quote the Joker from the best superhero movie ever made, “Some men just want to watch the world burn.”

Note about this exact idea coming soon.

Germany has been overbooked for decades with a strong saving culture, which is partly why German banks tried to offset their weak domestic returns via US real estate (via “super safe” AAA rated subprime CDOs), non-German sovereign debt (hello Greece!) and shipping (what could possibly go wrong?).

The net result is that DB and Commerzbank are quite weak because their foundation is in a country that promotes a very different banking environment than their neighbours.

Facebook : dairy farmer ::

Facebook user : cow ::

Advertiser : dairy customer ::

Personal information : milk

Public tax returns is a whole other thing. Might need analogies with the Matrix.

this is hilarious !! excellent analogy

Re : the NYT public declaration of taxes :So we have China with its Social Capital score and aggressive use of big data to monitor and influence all aspects of its citizens lives – resulting in a “Caesar” that has all the power and knows everything about you to keep you in line.

And in the US /developed world we have “Big Data” and all this so called “information for the good of the Public “ – allowing the “Caesars” to monitor and influence all aspects of their citizens lives….

Could just be me but it feels like both routes, rooted in supposedly opposing political and socio-economic philosophies, end up in the same destination?

I suppose, in the spirit of GoT being back: “Power is power?”