Central Bank Omnipotence Monitor – 1.31.2020

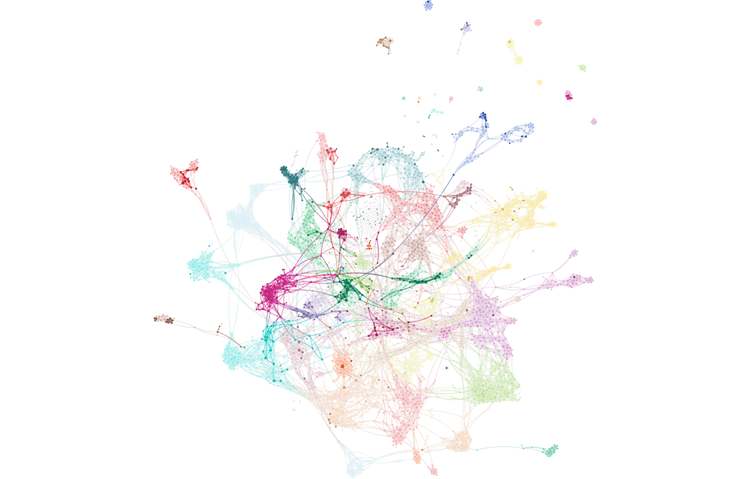

Attention on and cohesion of Central Bank macro narratives rose sharply in January. We believe that this is largely the result of a (hopefully!) short-term…

Attention on and cohesion of Central Bank macro narratives rose sharply in January. We believe that this is largely the result of a (hopefully!) short-term…

Access the Powerpoint slides of this month’s ET Pro monitors here. Access the PDF version of the ET Pro monitor slides here. Access the underlying Excel data here.…

Access the Powerpoint slides of this month’s ET Pro monitors here. Access the PDF version of the ET Pro monitor slides here. Access the underlying Excel data here.…

Access the Powerpoint slides of this month’s ET Pro monitors here. Access the PDF version of the ET Pro monitor slides here. Access the underlying Excel data here.…

Access the Powerpoint slides of this month’s ET Pro monitors here. Access the PDF version of the ET Pro monitor slides here. Access the underlying Excel data here.…

Access the Powerpoint slides of this month’s ET Pro monitors here. Access the PDF version of the ET Pro monitor slides here. Access the underlying Excel data here.…

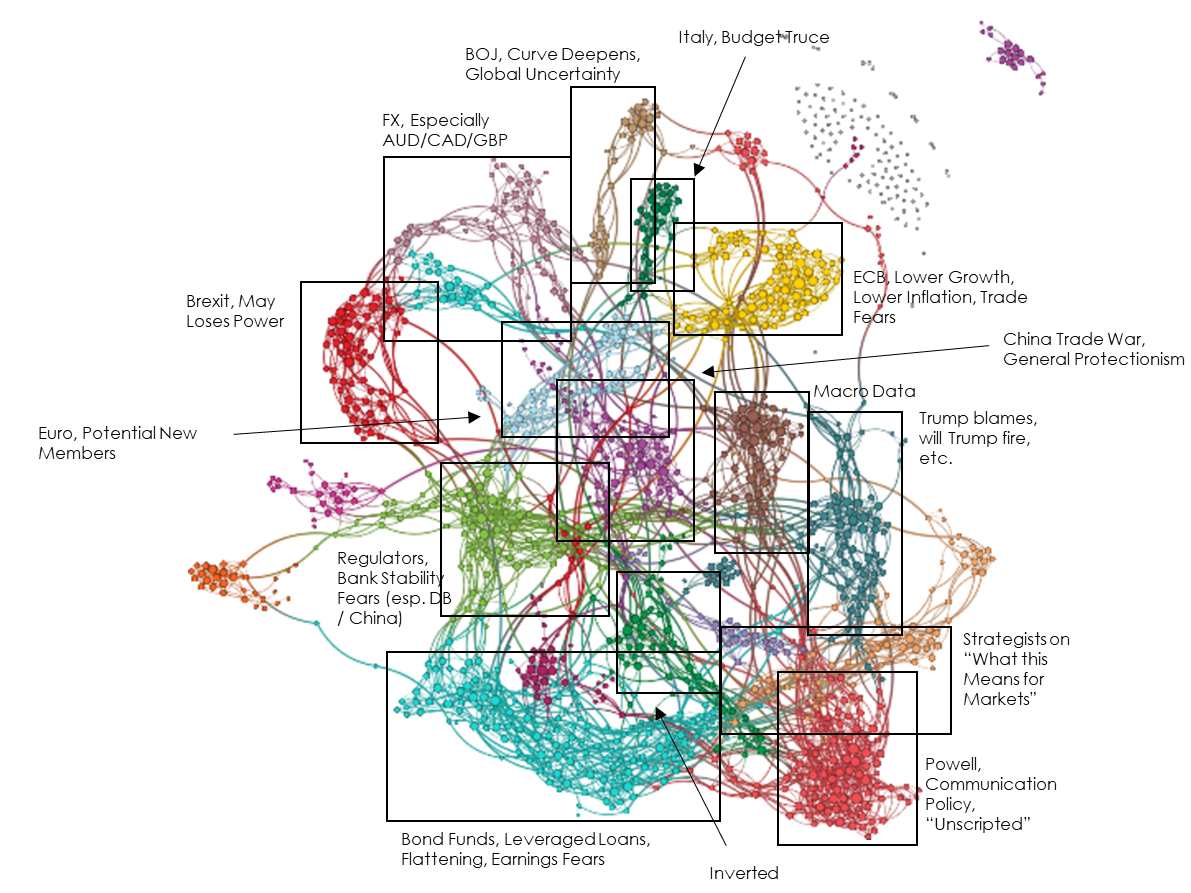

Editor’s Note (8.21.2019): We received a couple comments from readers that they found the different presentations for the charts and for the raw signal data…

Access the Powerpoint slides of this month’s ET Pro monitors here. Access the PDF version of the ET Pro monitor slides here. Access the underlying Excel data here.…

Access the Powerpoint slides of this month’s ET Pro monitors here. Access the PDF version of the ET Pro monitor slides here. Access the underlying Excel data here.…

Access the Powerpoint slides of this month’s ET Pro monitors here. Access the PDF version of the ET Pro monitor slides here. Access the underlying Excel data here.…

Access the Powerpoint slides of this month’s ET Pro monitors here. Access the PDF version of the ET Pro monitor slides here. Access the underlying Excel data here.…

Access the Powerpoint slides of this month’s ET Pro monitors here. Access the PDF version of the ET Pro monitor slides here. Access the underlying…

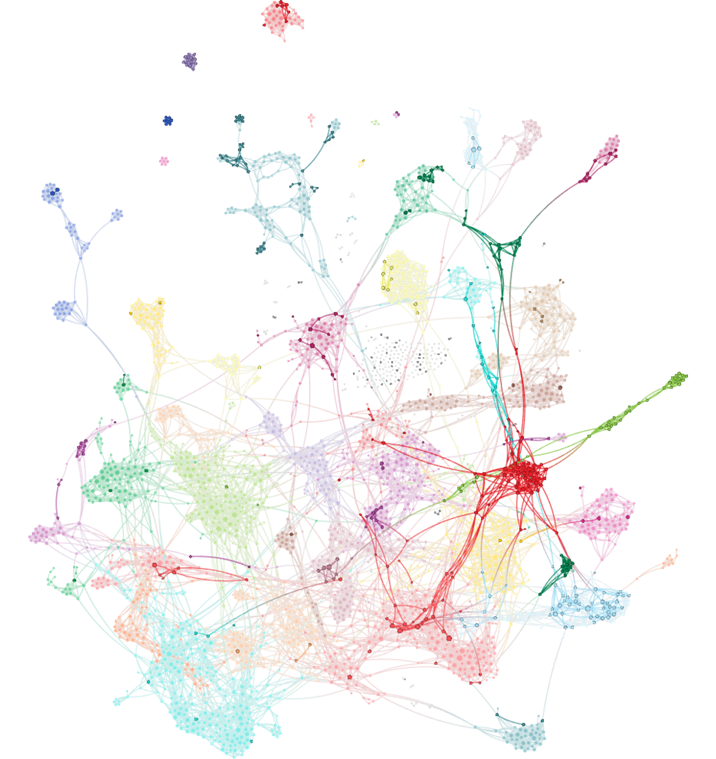

Access this month’s monitor slides in Powerpoint and in PDF. Access the data in Excel. Attention to central bank narratives continued to rise in January, to nearly the…

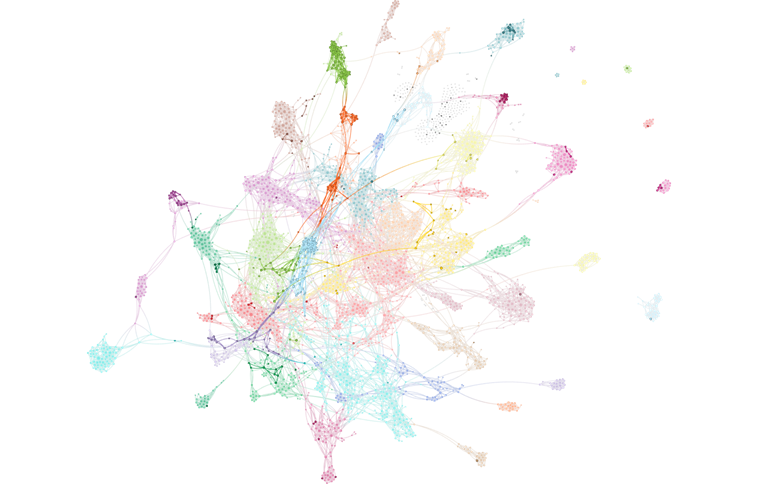

Access this month’s monitor slides in Powerpoint and in PDF. Access the monitor values in Excel. Attention to central bank narratives rose sharply in December, with a renewed attention…

Access this month’s monitor slides in Powerpoint and in PDF. Access the monitor values in Excel. While our slower smoothed measure has moved only slightly, our November point estimate…

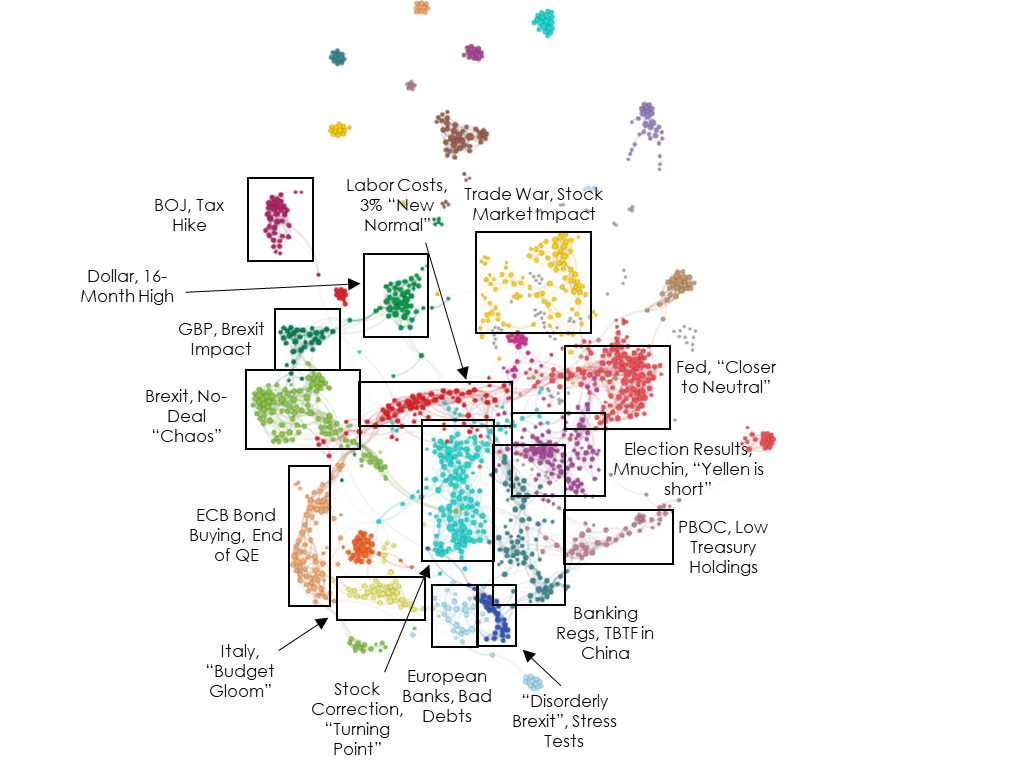

The Narrative of coordinated global central banking policy has been restrained for an extended period, including most of 2018. After a brief rise along with…