Join Us. No, Really.

Second Foundation Partners is looking for a new member of the team to help us spearhead the development of technologies for narrative analysis.

To receive a free full-text email of The Zeitgeist whenever we publish to the website, please sign up here. You’ll get two or three of these emails every…

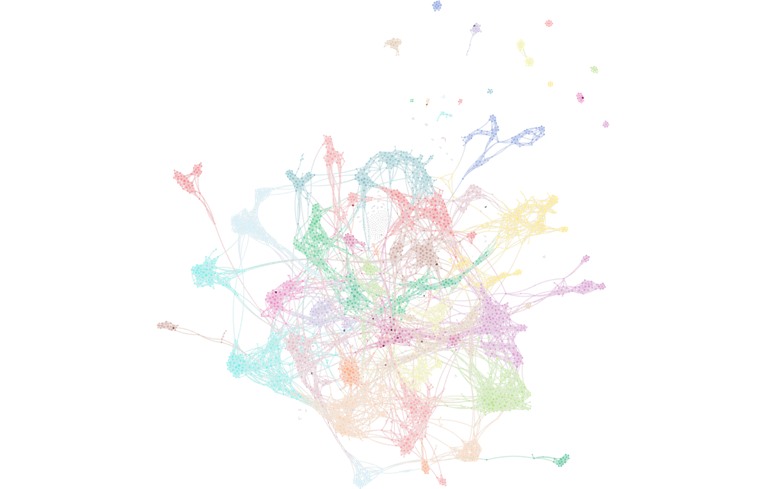

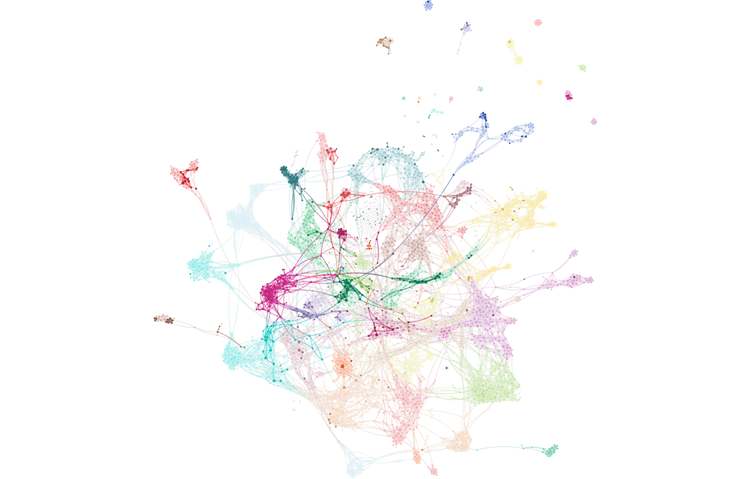

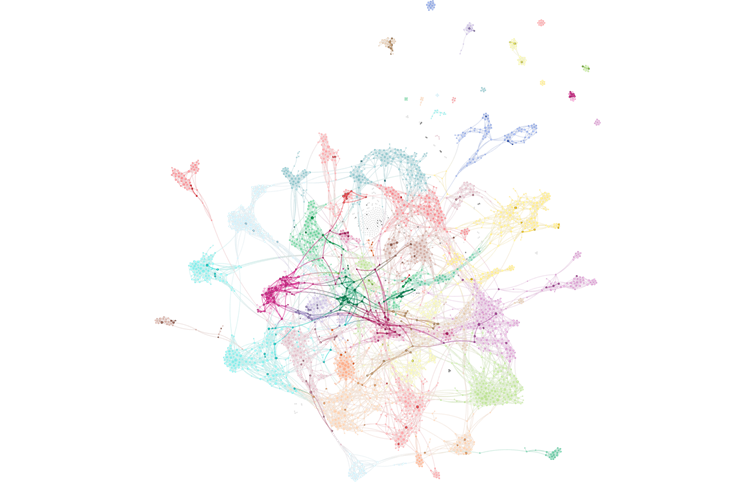

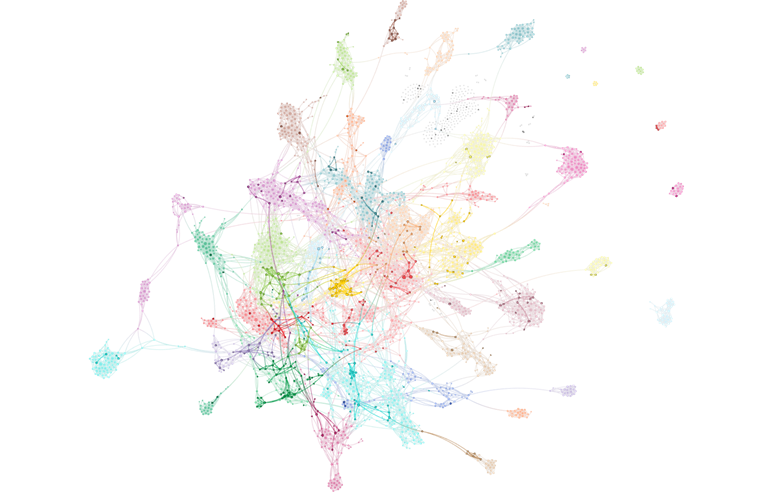

Like other topics, Recession narratives rose somewhat in attention and cohesion, but less dramatically than other categories. We believe that this is because coronavirus outbreak…

The decline in the strength of the Q4 Narrative of a risk of “collapse” in credit markets continued in January. Uniquely among our macronarratives, cohesion…

Like other topics, Recession narratives rose somewhat in attention and cohesion, but less dramatically than other categories. We believe that this is because coronavirus outbreak…

Attention on Trade and Tariffs topics rose somewhat, but the inclusion of coronavirus language proved a distraction to the stories being told about them rather…

Attention on and cohesion of Central Bank macro narratives rose sharply in January. We believe that this is largely the result of a (hopefully!) short-term…

Attention on inflation rose rapidly and surprisingly in January, we think in response to two developments: The very modest emergence of inflation in even heavily…

Access the Powerpoint slides of this month’s ET Pro monitors here. Access the PDF version of the ET Pro monitor slides here. Access the underlying Excel data here.…