The Zeitgeist | 2.13.2019

In the 8th or extra innings (what about the 9th?), allocations to alternatives, fixed income ETFs, offensive hacking and "markets up on trade deal hop…

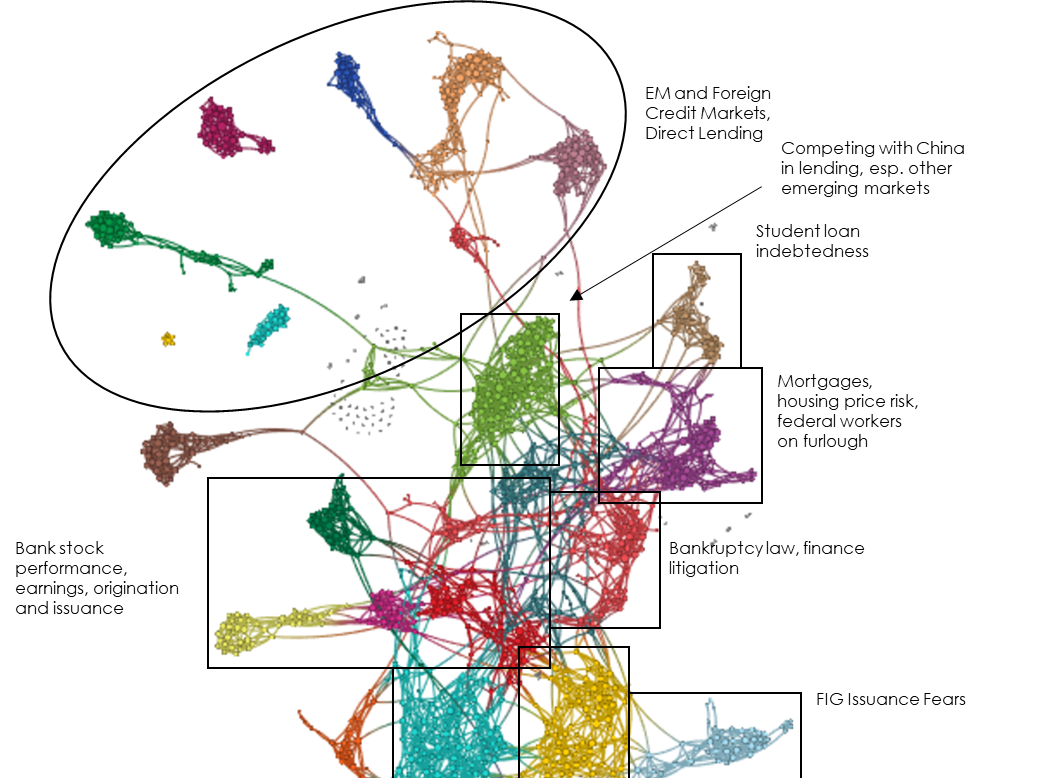

Access this month’s monitor slides in Powerpoint and in PDF. Access the data in Excel. The attention on credit and credit cycles has increased slightly, but most of…

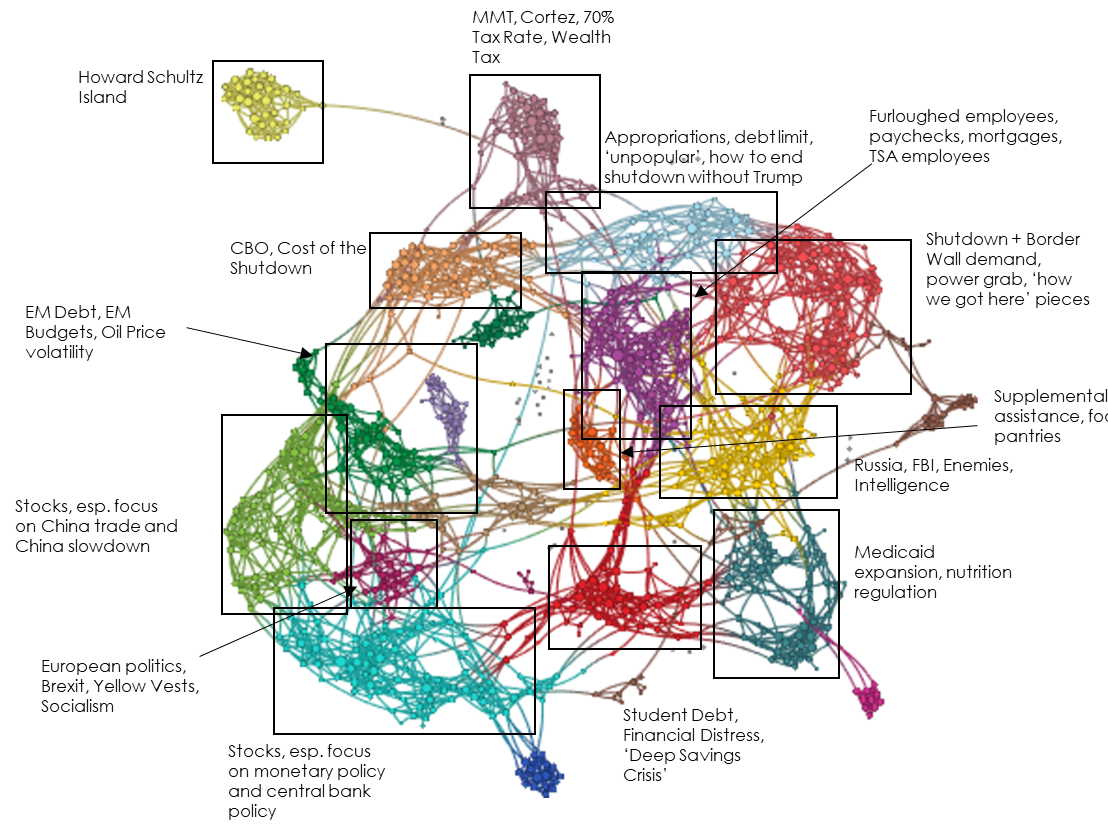

Access this month’s monitor slides in Powerpoint and in PDF. Access the data in Excel. Attention to fiscal policy narratives has dramatically increased in January. The shutdown (and…

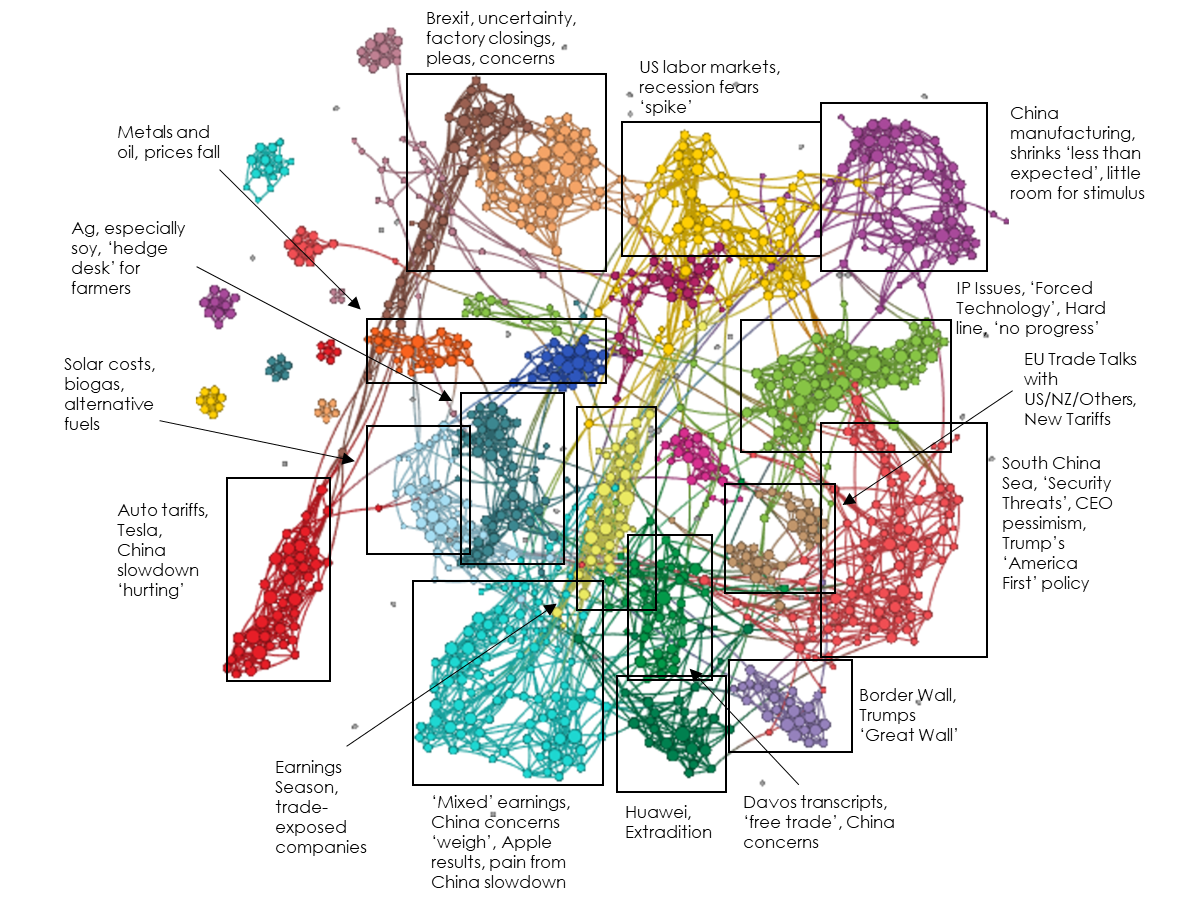

Access this month’s monitor slides in Powerpoint and in PDF. Access the data in Excel. Attention on Trade and Tariffs is now as high as we have measured…

Access this month’s monitor slides in Powerpoint and in PDF. Access the data in Excel. Attention to central bank narratives continued to rise in January, to nearly the…

Access this month’s monitor slides in Powerpoint and in PDF. Access the data in Excel. Our attention measure for Inflation narratives rose somewhat in January, probably the result…