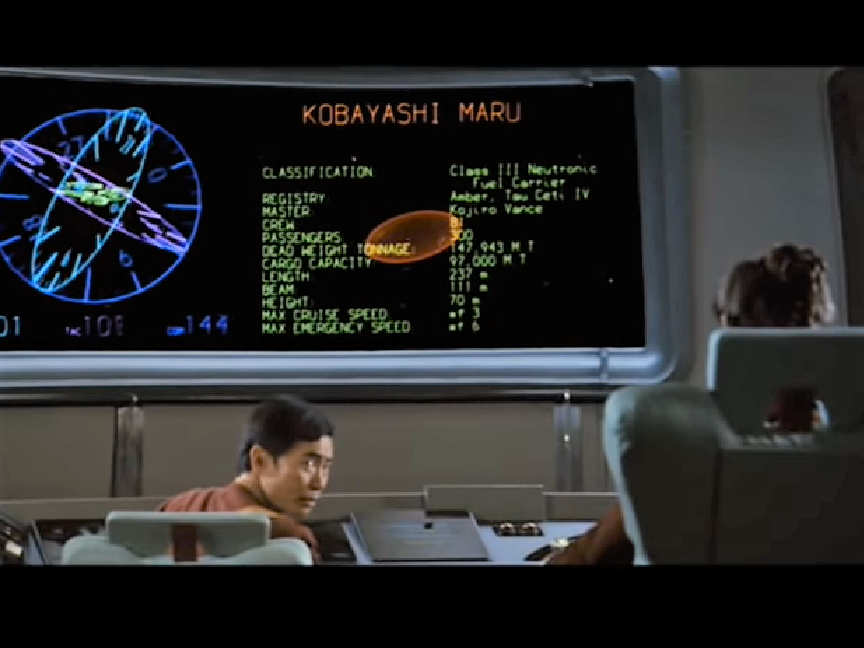

When facing a no-win scenario, sometimes the only rational choice is for our advisers and managers to change the conditions of the test. That doesn't …

Food and retailing are top of mind (and...bullish?), trade continues to dominate content and commentary, and a hero rides in to protect the Lu Ann Pla…

Like it or not, the 2020 election season has begun. But I've got good news for you: someone has The Answer for the political center, and he'd very muc…

Last Halloween the hipsters over at Salesforce.com turned their new San Francisco building into a giant Eye of Sauron. I keep waiting for someone to t…

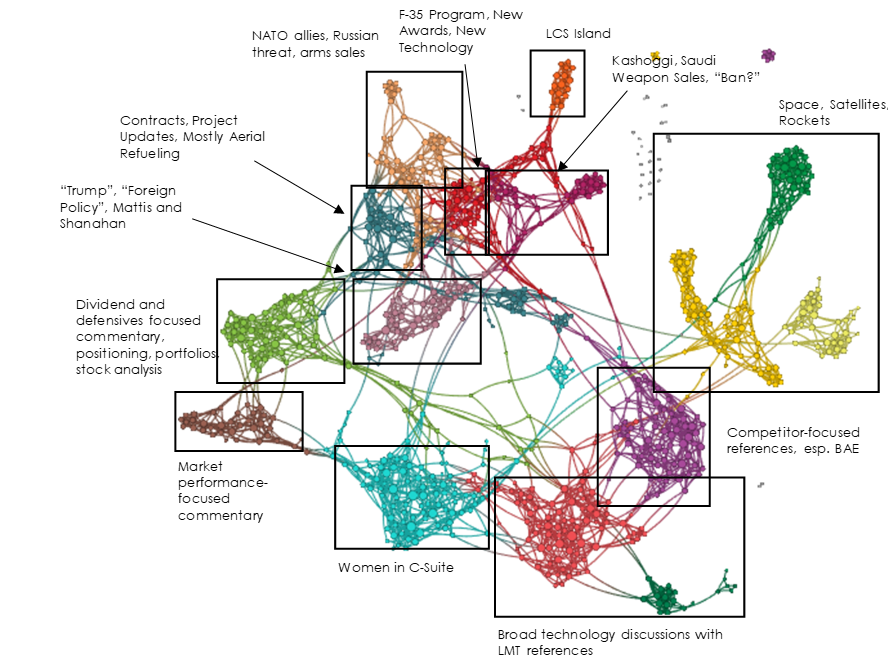

With aerospace and defense in the spotlight, we turn our own spotlight to the sector. We find a generally weak narrative structure with a lot of vulne…

When an inflation regime shifts, the only question that really matters for your investments and your business model is this: do you have pricing power…

A generation of investors has Paul Volcker to thank for almost 40-years of slowly falling rates. He handed countless baby-boomers a free 100 points of…

The gyre widens again, and if we are not careful, it will force us into positions that require us to deny the basic humanity of our fellow citizens. R…

We use cookies to optimize our website and our service.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.