Why Hope?

It's easy to feel like we need more than hope to pass through troubling times, and it's usually true. But sometimes hope is exactly what we need.

After several months of increasing cohesiveness around an inflation-is-coming Narrative, attention to the topic has been tapering in early Q4 Right now we think this…

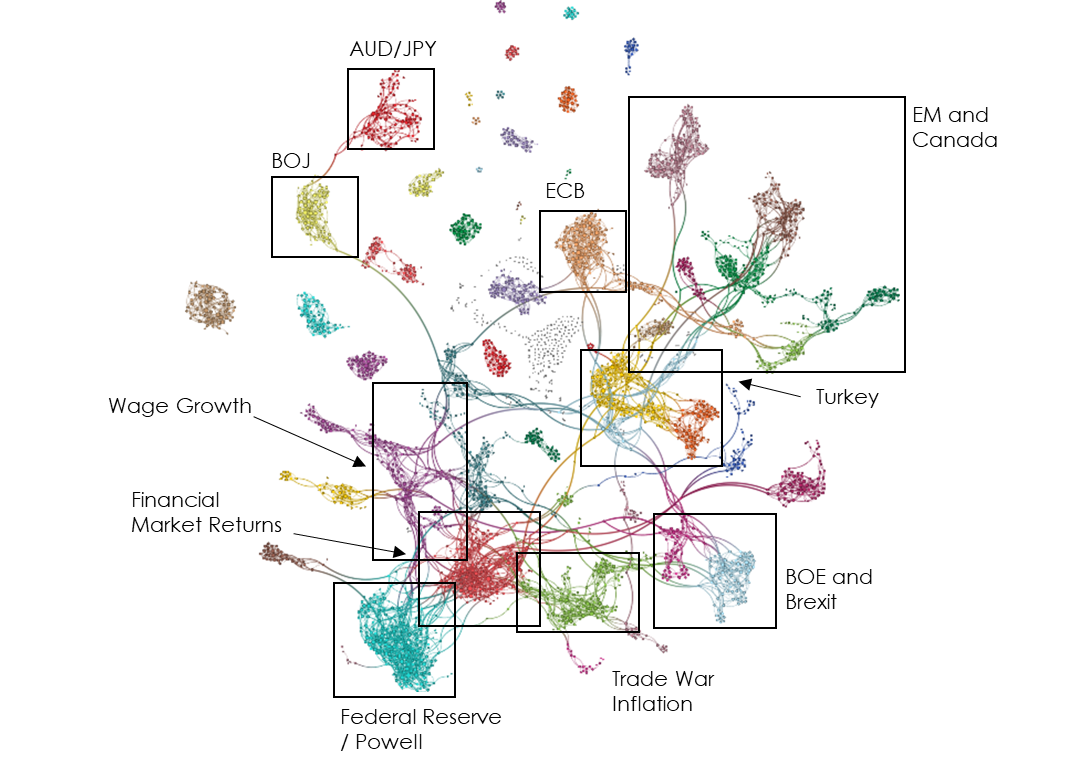

The Narrative of coordinated global central banking policy has been restrained for an extended period, including most of 2018. After a brief rise along with…

While it is only a single data point, our October attention measure rose from its very low base over the prior three months. Our aggregate…

After climbing as usual (and, we think, in more muted fashion) in connection with mid-term elections, attention to US Fiscal Policy narratives ticked down modestly…

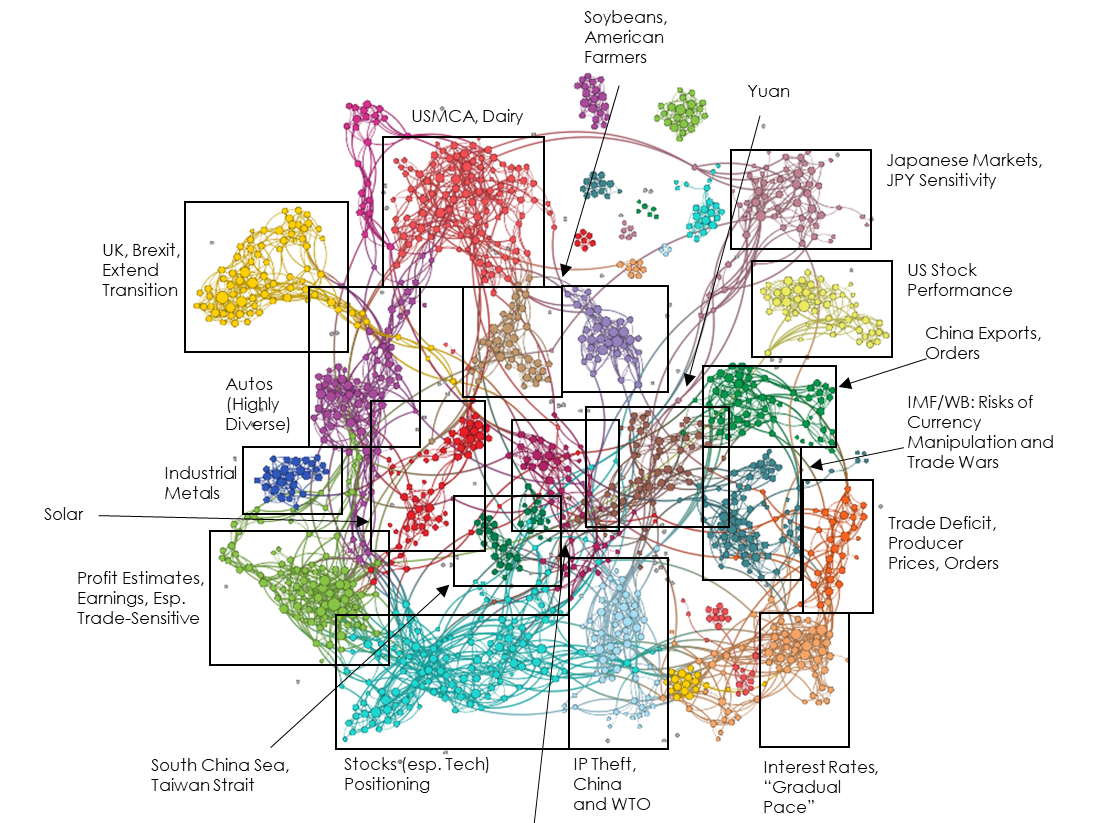

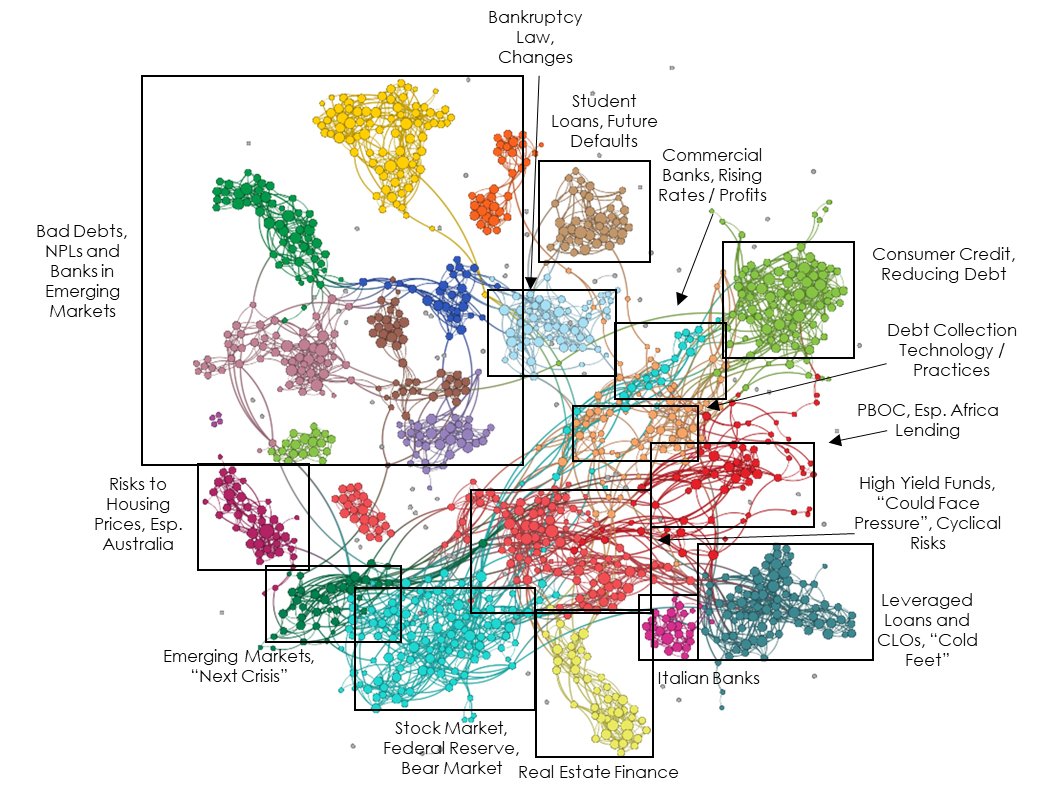

While articles including key credit terms continued to rise in October, their internal coherence continued to fall. This means that stories tended to cover individual…